How Could Inflation Affect Your Retirement?

In recent months, Procter & Gamble has raised prices for its Tide, Gain, Downy and Bounce product portfolio. It recently announced that this spring, consumers also will start paying more for many of its personal health care brands. The company is hardly alone. Nestle, Danone, Unilever and other consumers goods giants say their prices will continue to rise due to high inflation.1

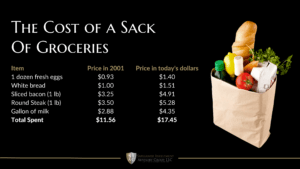

Inflation is a two-faced beast. On one side, a healthy increase in prices indicates a growing economy. However, when prices increase substantially over a short period of time, it can signal other problems. The obvious problem is the world is still in the throes of a pandemic, and periodic flare-ups cause supply chain disruptions and inventory shortages. Also, the Federal Reserve has altered its monetary policy to allow higher levels of inflation in order for slow-growing areas of the economy to benefit. The sum total of these factors is that, right now, we are seeing greater inflation than we have in more than 20 years.

The thing that makes inflation more controversial than other economic factors is that it has an immediate impact on household budgets in a way that global trade agreements and adjusted interest rates typically do not. While, in time, fiscal and monetary intervention will set in to curb short-term price hikes, today’s environment is a great reminder of just how harmful rising prices can be on a household budget. While many working families can cut back or alter product choices, a lot of retirees already made those types of adjustments to their budgets when they stopped working. That makes it harder for those living on fixed incomes to adjust to rising consumer prices.2

For example, the value of a pension declines when inflation climbs at an annual rate that exceeds the pension yearly increase. Let us know if you’d like to find new ways to supplement your household income as inflation rises during retirement.

If you look at inflation in the United States from a historical point of view, today’s rising prices are not nearly as bad as they used to be. In fact, baby boomers lived through “The Great Inflation” era from 1965 to 1982 — so they are well aware of the devastating impact of runaway inflation. A recent survey discovered that people nearing retirement view today’s inflationary hike as a cautionary tale and are planning for the worst:3

- 33% expect to need a bigger nest egg for retirement

- 36% say the pandemic has reduced or will reduce their standard of living

- 21% say they will need to work longer and delay their retirement to make ends meet

- Although most participants say their portfolio has outperformed in recent years, most don’t think it will be enough to fund their retirement needs

As for steps they are taking, baby boomers and near-retirees are boosting their nest eggs by reducing their current spending (62%), taking a part-time job (32%), increasing investments (25%), delaying retirement (21%), and adopting a more conservative withdrawal rate from their savings (14%).4

Unfortunately for many pre-retirees, their retirement savings are not where they need to be — especially if they hope to offset inflation while living on a fixed income for 20-plus years. Not only does today’s typical boomer household still have an average of $28,672 in debt, but the median 401(k) account balance is $61,738 for 55- to 64-year-olds. The lack of retirement preparedness is even worse for women. According to a Census Bureau report, approximately 50% of women ages 55 to 66 have no personal retirement savings (compared to 47% of men).5

Are you in need of any financial advise? We are here to help. Click here to schedule a 15-minute strategy call with one of our financial experts.

1 Avery Hartmans. Business Insider. Jan. 19, 2022. “P&G warns that price hikes for everyday products aren’t over yet.” https://www.businessinsider.com/procter-gamble-price-increases-laundry-detergent-healthcare-products-inflation-2022-1. Accessed Feb. 2, 2022.

2 Peter G. Peterson Foundation. April 14, 2021. “What is inflation and why does it matter?” https://www.pgpf.org/budget-basics/what-is-inflation-and-why-does-it-matter. Accessed Feb. 2, 2022.

3 Megan DeMatteo. Money Talks News. Oct. 15, 2021. “The Top Reason Baby Boomers Are Putting More Away for Retirement.” https://www.moneytalksnews.com/slideshows/the-top-reason-baby-boomers-are-putting-more-away-for-retirement/. Accessed Feb. 2, 2022.

4 Ibid.

5 Jason Lalljee and Hillary Hoffower. Business Insider. Jan. 19, 2022. “Boomers don’t have nearly enough retirement savings, especially women.” https://www.businessinsider.com/boomers-dont-have-retirement-savings-women-have-less-than-men-2022-1. Accessed Feb. 2, 2022.

We are an independent firm helping individuals create retirement strategies using a variety of insurance and investment products to custom suit their needs and objectives. This material is intended to provide general information to help you understand basic financial planning strategies and should not be construed as financial or investment advice. All investments are subject to risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information contained in this material is believed to be reliable, but accuracy and completeness cannot be guaranteed; it is not intended to be used as the sole basis for financial decisions.

Ready to Take The Next Step?

For more information about any of the products and services listed here, schedule a meeting today or register to attend a seminar.